Of Bodas and Batteries: The Future of Kenya’s EV Market

Kenya’s electric vehicle sector is speeding ahead—but the story is uneven

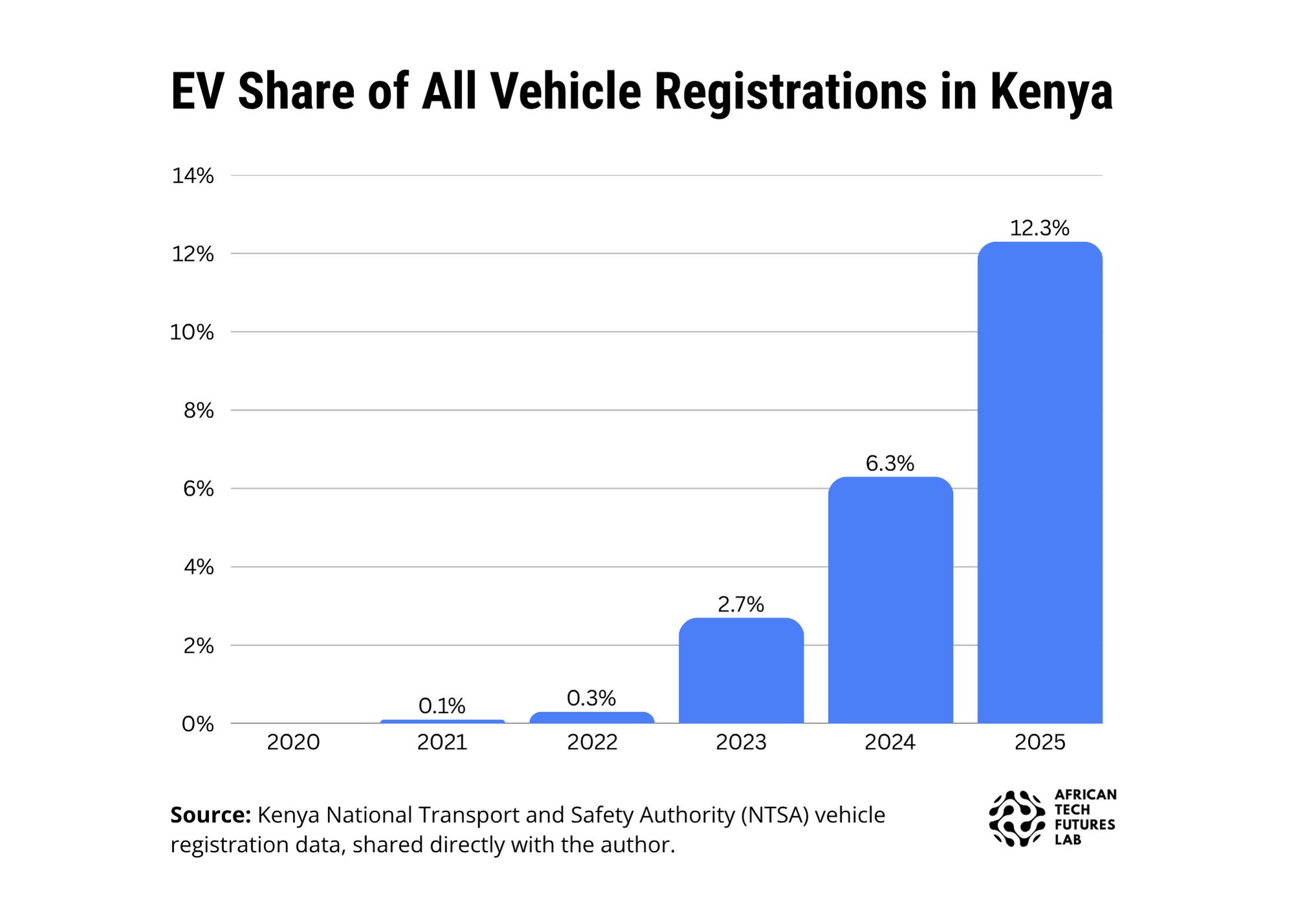

Figure 1: EV share of all vehicle registrations in Kenya.

Kenya’s electric vehicle (EV) market is growing rapidly, with EVs going from near-zero to more than 12% of new vehicle registrations over the past five years (Figure 1). Much of this growth has been driven by the e-motorcycle segment, which accounted for one in six motorcycle registrations in 2025 (Figure 2). Kenya has long been one of the closest watched EV markets on the continent, and this new data shows that the optimism is not unwarranted.

But these headline numbers need to be read carefully. EVs still accounted for just 0.12% of Kenya’s total vehicle fleet as of 2024, according to recent estimates. That distinction matters, as registration shares capture the direction and speed of new adoption, while fleet shares show how much of the vehicle stock has actually turned over. Kenya is moving quickly on the first measure but remains at a very early stage on the second. The transition is also highly uneven across vehicle segments, and future growth is contingent on managing several important chokepoints, particularly around charging and finance.

This memo digs into these dynamics in each of the key vehicle segments, providing insight into the constraints and opportunities that will shape the next phase of Kenya’s EV transition.

Electric Motorcycles: Driving Kenya’s EV Transition

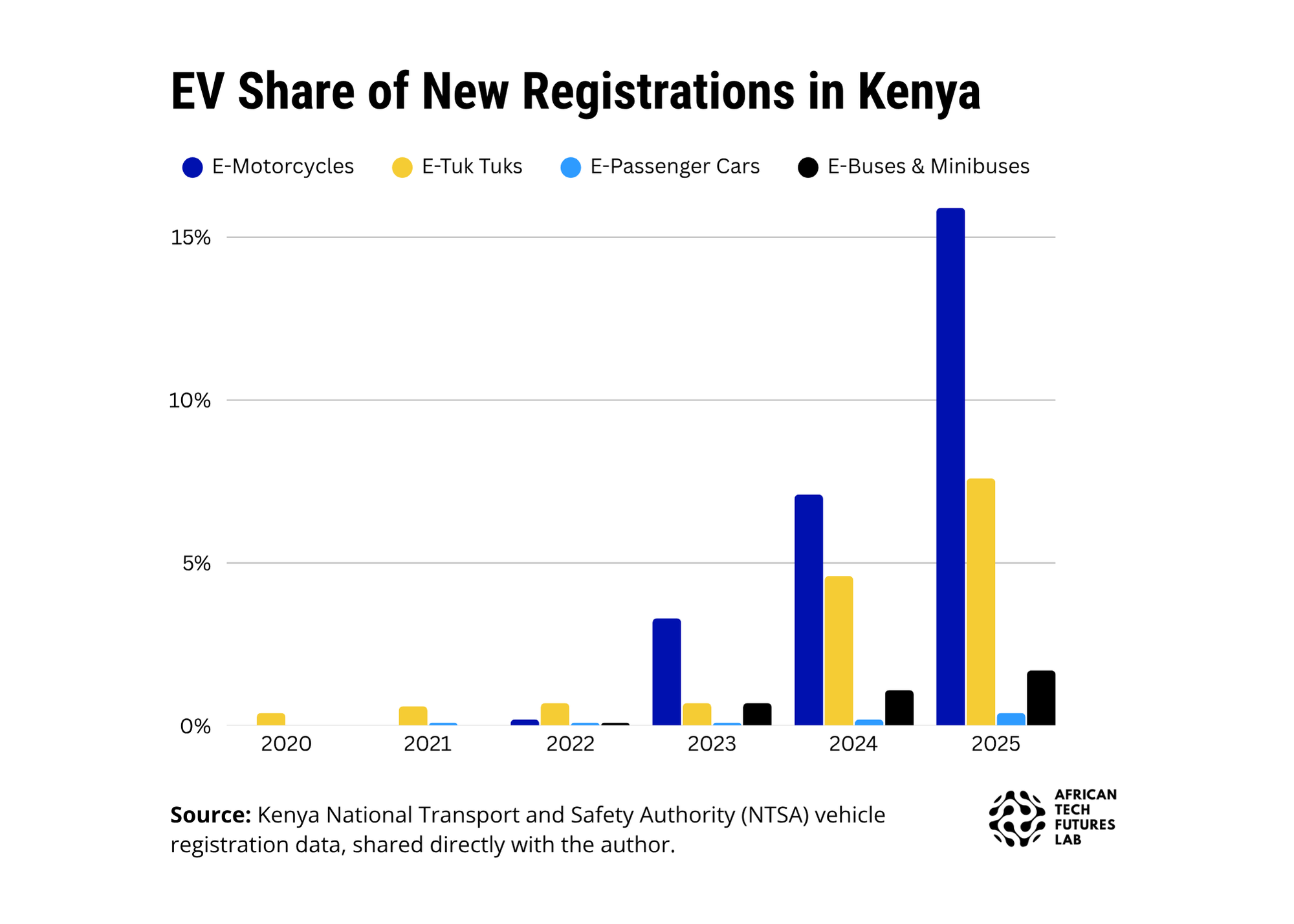

Figure 2: EV share of new registrations by vehicle segment.

Looking at EVs share of total new vehicle registrations disaggregated by vehicle segment, it is clear that Kenya’s EV story is dominated by electric motorcycles. From near-zero shares before 2023, e-motorcycles have grown to claim one in six of all new motorcycle registrations by 2025.

This growth in the e-motorcycle segment is all the more impressive given the broader turbulence in Kenya’s motorcycle market over the past five years. Between 2021 and 2024, the motorcycle market itself collapsed, plummeting from nearly 300,000 registrations to less than 70,000. The combination of a weak shilling, higher fuel costs, and squeezed household incomes hit internal combustion engine (ICE) motorcycle sales hard [1]. Demand is now recovering to the earlier baseline, with the overall motorcycle market more than doubling in 2025. E-motorcycles grew far faster still, increasing nearly fivefold over the same period.

This growth is not evenly spread, however. For now, the e-motorcycle boom is concentrated in Nairobi and peri-urban markets, where dense populations, short daily trips, and more developed battery swap-infrastructure help facilitate the switch to electric. Rural electrification, on the other hand, remains an open question to watch. This concentration is likely to lead to a slowdown in sales share growth once urban areas are saturated, particularly given the higher performance demands (both vehicle range and power) and lower returns on charging infrastructure in rural areas.

Battery Supply Chains are the First Scale Test for Kenya’s E-Motorcycle Sector

The same growth that makes Kenya’s e-motorcycle market exciting is also creating its own problems. Notably, motorcycle sales have outstripped available batteries in some cases. At least two battery swap networks operating in Kenya, the dominant model for e-motorcycle energy delivery in the country, experienced battery shortages in the beginning of the year. Rapid uptake in 2025 at the EV startup Spiro in particular—estimated to make up nearly three-quarters of e-motorcycle registrations in Kenya last year [2]—has outpaced battery procurement and logistics. Tired of queuing at swap stations, riders were waking up early to try to get fully-charged batteries earlier than their colleagues. The solution is straightforward: deploy more batteries on the network. However, the lead time from battery purchase order to availability in swap stations can run several months. This is an early supply chain stress test for the industry, and how operators respond will matter for whether rider confidence in the electric model holds. While these battery shortages have since been alleviated, the same conditions can crop up again.

The Rest of the Market

Motorcycles dominate Kenya’s EV story, but the other segments deserve attention.

Three-Wheelers: A Small But Growing Market

Closest behind motorcycles in Kenya’s electrification transition are tuk tuks—three-wheeled passenger and cargo vehicles—with electric tuk tuks accounting for 7.6% of new tuk tuk registrations in 2025. However, the tuk tuk market in Kenya is quite small and mainly concentrated in the coastal region, so this 7.6% figure translated to only 517 electric tuk tuks. Tuk tuks have many of the same advantages of motorcycles, such as smaller batteries and high daily mileage. Sales shares should thus continue to grow meaningfully, even if volumes in this vehicle class remain relatively modest in the Kenyan context. Unlike Asian markets like India, where the three-wheelers currently dominate the transition to electric mobility, tuk tuks will remain in the shadow of Kenya’s electric motorcycle revolution.

Buses and Minibuses: Few in Number, Big in Impact

Electric buses and mini-buses only started appearing meaningfully in the data from 2023, tripling in a year to reach 106 new registrations in 2025 or nearly 2% of total bus and mini-bus registrations. These numbers are comparatively small—106 e-buses versus 20,000 e-motorcycles in the same year—but their economic weight is larger than the unit count suggests.

A 34-seat electric bus can cost roughly $100,000 to $200,000, making each purchase a substantial investment. Operators who have switched to electric buses report dramatically lower operating costs, including savings in the range of 70-80% on fuel and maintenance. Some report netting KES 5,000–10,000 (~$40–$80) more per day than they did on diesel. The segment is likely to remain small in the near term given the capital required, but its economic significance to early movers is disproportionate to its size.

Passenger Cars: Used ICE Imports Remain Entrenched

Electric passenger cars remain barely visible in the data, accounting for only 0.4% of passenger car registrations in 2025. This reflects tough competitive realities: Kenya's car market is dominated by used imports selling for under $10,000, and new EVs strain to go head to head on price in a market shaped by second-hand Japanese vehicles.

Given current trends, electrification of private cars is not a significant near-term phenomenon in Kenya. The main exception may be the Nairobi-based ride-hailing segment, who see greater savings due to higher daily mileage and have a stronger economic case for switching.

What to Watch Next

Kenya is moving rapidly on vehicle electrification, there is no doubt about that. The harder questions—about who benefits, whether cars and buses can match the motorcycle curve, and whether the infrastructure and supply chains can keep pace—are only beginning to come into focus. A few important trends to watch include:

Battery availability: Whether operators can finance and procure enough batteries ahead of demand.

Charging pricing and transparency: Battery-swap users have little transparency into the price per energy purchased, something that could change with new tools.

Network coverage and interoperability: As exclusive networks grow, partnerships or even mandated interoperability could upend the field and boost access for users.

Affordability and ownership: Battery-swapping and pay-as-you-drive models, including new innovations around battery-swapping for small-cars, could improve affordability and uptake.

EV taxation: The Kenyan president has declared import duty exemptions for the first 100,000 EVs, which could amplify sales in the short term.

Better public data: Clearer, consistent, disaggregated data across the continent would sharpen the picture.

[1] Author interview with motorcycle financing investor.

[2] NTSA data, shared directly with the author.